Don’t burn out your battery chasing pennies — here’s why energy trading hurts your wallet

Buying a Battery Just for Energy Trading? That’s Like Buying Tyres for Burnouts

Every now and then, someone proudly tells us they’re getting a solar battery so they can “make money” trading power back and forth with their retailer. The idea is simple: charge the battery cheap, discharge it when the retailer pays more, and profit!

Except… in the real world, that’s about as smart as buying a set of expensive high-performance tyres just to do burnouts in your driveway. It’s fun in theory, but it’s expensive, it’s wasteful, and it leaves you with a lot less tread than you started with.

Better to buy new tires for getting from A to B; and better to get a solar battery for energy resilience and decreasing demand on the grid in the few hours after sunset.

A Common Bait And Switch

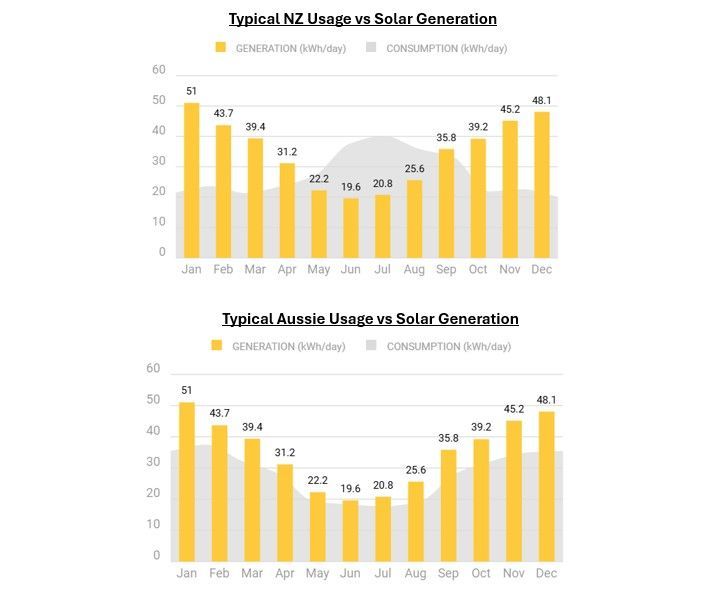

One of our favourites is when clients say: “I want to make sure my battery is charged by 5 pm so I can export the energy for 20 something cents."

Great idea… if your goal is to make less money. Because during those same hours, the import rate could be around 40c.

So let’s do some Year 10 maths:

- If you use your own stored energy between 5pm - 9pm, you’re avoiding paying 40c/kWh (ish).

- If you export it, you might be lucky enough to earn 20 - 30c, depending on your retailer.

That’s right — you’re literally selling something for less than it’s worth to you.

That’s not energy trading. That’s a slow leak in your wallet.

The Real Cost of “Burnouts”

Batteries have a finite number of cycles in them. Every time you charge and discharge, you’re wearing down the chemistry.

Most warranties cover one full cycle per day. Go harder than that with energy trading, and you’ll hit two problems:

Warranty woes – your warranty will 'run out of tread before' 10 years rolls around.

Premature capacity loss – that shiny 12 kWh battery might be holding 9 kWh before you know it.

It’s a bit like owning a V8. You can accelerate quickly, and hit some high speeds. But floor it too often and you end up paying for it in trips to both the gas station and tyre shop.

Why the Payback Just Doesn’t Stack

Let’s be generous and say you’re trading at a net gain of 22 c/kWh.

With a 12 kWh battery, you might make $2.64/day, or $963/year. That’s before you factor in efficiency losses (you don’t get 100% of what you put in) or degradation.

If the battery cost you $15,000, that’s a 15-plus-year payback — if the battery isn't limping for the last leg of the marathon.

Smarter Uses for a Battery

Instead of playing amateur energy trader, use your battery for:

- Self-consumption – keeping your own power bills down by using what you generate.

- Backup power – so when the lights go out, yours stay on.

- Load shifting – charging cheap before the morning peak time to avoiding paying the expensive peak morning rate, typically between 7am and 9-11am.

Those uses get you real value without turning your battery into a worn-out set of burnout slicks.

Final Thought

If you’re buying a solar battery purely to export for a few cents’ gain, you’re not trading — you’re giving the retailer the better deal. Keep the 35c power for yourself, skip the “tyre burnouts,” and let your battery live a long, productive life.